Pete Townshend was just 20 when he wrote the immortal line, “Hope I die before I get old”, for The Who’s 1965 anthem My Generation. It was an admirably bold commitment for someone who had not yet encountered lower-back pain, compound interest, or the administrative complexity of claiming from a medical aid.

Townshend, born in May 1945, is now 81, which does suggest that youthful manifestos should come with the same disclaimer as long-term economic forecasts: circumstances may change. He later explained that by “old” he had meant something closer to becoming very rich, complacent, and bourgeois, which is clever, because it transformed a failed actuarial prediction into successful social commentary.

The Who also wrote The Kids Are Alright, and between those two song titles lies practically the entire field of generational economics. Are the kids alright? Are their parents alright? Are their grandparents rather more alright than actuarially necessary? And, most importantly, who owns the house in which everyone is arguing?

The youth-versus-age debate is itself ancient. Oscar Wilde observed that “the old believe everything; the middle-aged suspect everything; the young know everything”. Saki improved on this by noting that the young have aspirations that never happen, while the old have memories of things that never happened. La Rochefoucauld supplied the finishing blow: old men offer good advice partly because they can no longer set bad examples.

All of which should make us suspicious whenever one generation rises to accuse another of ruining civilisation. The great advantage of a generational argument is that everybody eventually changes sides without having to admit they were wrong.

Yet the latest accusation deserves attention. American academic, entrepreneur, and blogosphere foghorn Scott Galloway has revived his argument that the United States is conducting a “war on the young”. His case is that older Americans have accumulated a disproportionate share of the national wealth, inflated the value of their houses and shares, protected their pensions and healthcare, restricted access to housing and elite universities, and then presented the bill to their children.

“Keep me rich, on your credit card,” is how Galloway summarises the arrangement. He says the social contract - work hard, obey the rules and become better off than your parents - has been broken. Young Americans enter adulthood with student debt, expensive housing, and weak labour-market prospects, while older asset owners enjoy the fruits of decades of rising property and equity prices.

There is plenty in this that is right.

Housing policy in many successful cities has become an insiders’ protection racket conducted through zoning regulations, planning objections, and concerned residents’ associations. Existing homeowners discover an intense affection for neighbourhood character immediately after acquiring the last available house. Universities boast about rejecting almost everyone, as though educational scarcity were evidence of educational excellence. And governments routinely make promises to current voters that will be financed by people who have not yet voted, or in some cases been born.

There is also strong evidence that the American escalator has slowed. Research by Opportunity Insights estimates that about 90% of Americans born in 1940 grew up to earn more than their parents. For those born in the 1980s, the figure is closer to 50%. Greater inequality in the distribution of growth explains much of the decline.

But Galloway’s “war” metaphor does some suspiciously heavy lifting.

His argument often compares today’s elderly people with today’s young people, rather than comparing different generations at the same age. Naturally, a 75-year-old generally owns more than a 25-year-old - one has had half a century to acquire a house, shares and a pension; the other has had half a decade to acquire an air fryer and an alarming debit order from a gym.

Once one makes the proper age-adjusted comparison, the American evidence becomes much less apocalyptic. The St Louis Federal Reserve estimates that younger American households had, on average, $1.23 in wealth for every dollar held by Gen X at a similar age, and $1.35 for every comparable boomer dollar. Another Federal Reserve study found that millennials aged 36 to 40 had real median post-tax, post-transfer household incomes 18% above the preceding generation at the same age.

That does not mean the young are swimming in economic opportunity. Averages conceal ferocious inequality, and younger Americans remain less likely to own homes. But it suggests that the primary divide may not be young against old. It may be owners against non-owners, heirs against non-heirs, graduates of useful courses against borrowers who paid enormous sums for weak qualifications, and people born into flourishing cities against people trying to enter them.

Student debt is a good example. It is usually presented as though the debt financed nothing at all. Yet a university qualification is an economic asset, even though it cannot be repossessed and parked outside the bank. In 2024, an American worker with a bachelor’s degree earned median weekly pay of $1,543, against $930 for someone with only a high-school diploma, and also faced a lower unemployment rate.

The real victims of student debt are disproportionately those who borrow but do not graduate, attend poor institutions,, or obtain qualifications with weak labour-market returns. The existence of bad educational investments does not make all education a generational swindle.

There is another inconvenient matter: diminishing returns.

It is relatively easy to become visibly better off than parents who grew up without electricity, secondary education, modern medicine, or private transport. It is much harder for every child of a comfortable professional household to earn more than two already successful parents. At a certain level of development, the arithmetic becomes uncooperative. Progress continues, but it arrives as better cancer treatment, faster communications, safer cars, and more leisure - not necessarily as a salary twice as large as Dad’s.

The first generation to get a refrigerator experiences a revolution. The next gets a refrigerator with an internet connection, which is progress of a sort, although nobody has yet explained why the refrigerator needs to know my password.

This is why the argument needs to be translated very carefully into South Africa.

At first glance, the local evidence appears to support Galloway. Wealth rises dramatically with age. Research using tax records, surveys, and national balance sheets found that South Africans aged 20 to 25 had average wealth below one-quarter of the national adult average. Those aged 50 to 55 had between one-and-a-half and twice the average, while even people older than 75 remained more than 50% above it.

The fiscal system also produces a startling comparison. The old-age grant is now R2,400 a month. The child-support grant is R580. In the 2026/27 budget, the state allocated about R121.8bn to old-age grants and R89bn to child support, despite old-age grants reaching roughly 4.3-million people and child grants reaching about 12.6-million.

Put like that, South Africa appears to have made an interesting moral choice: it values a poor person more highly after their 60th birthday than before their 18th.

But this is not quite fair. The old-age grant is intended to provide most of an indigent adult’s income. The child-support grant is intended to supplement the resources of a caregiver. Children also receive public education, school nutrition, and healthcare. The 2026 budget allocates R344.7bn to basic education and R527.2bn to learning and culture more broadly.

More importantly, South Africa’s old people are not a uniformly prosperous occupying force. Grants were the principal source of income for 60.1% of households headed by an older person in 2024. Many have little pension wealth, no meaningful savings, and a house that may be fully paid off but produces no cash.

And the money does not politely stop at the pensioner.

The South African old-age grant is one of the country’s most effective family-support programmes, although it is not officially described that way. It feeds unemployed children, grandchildren, and sometimes great-grandchildren. Esther Duflo’s famous research found that pensions paid to grandmothers improved the nutritional outcomes of girls living in the household. The elderly recipient was not absorbing the transfer; she was distributing it.

This is the point at which the neat American generational morality play collapses in a heap.

The South African grandmother receiving R2,400 a month is not the local equivalent of a Florida retiree guarding a million-dollar house and a tax-advantaged investment portfolio. She may be the only person in the household with a reliable income. Taking money from her in the name of generational justice could result in less food for the supposedly favoured young.

Nor is age the main organising principle of South African wealth inequality. The same wealth research found that within every broad age category - from people under 40 to those over 60 - the richest 10% owned more than 85% of the group’s wealth, and the richest 1% more than 55%. The difference between rich and poor South Africans is vastly greater than the difference between old and young South Africans.

A wealthy 28-year-old who has inherited a house, education and family connections is not economically allied to an unemployed 28-year-old in Lusikisiki merely because both know who Tyla is. Likewise, a poor pensioner in an extended household has little in common with a retired executive drawing income from several properties and a large retirement fund.

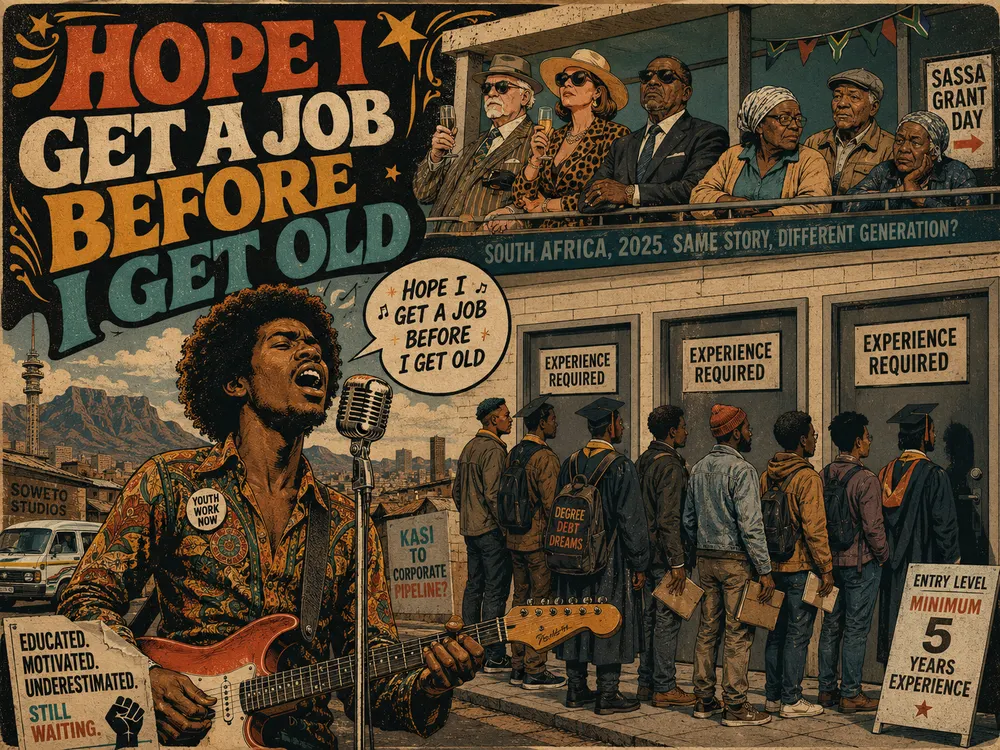

South Africa’s true conflict is not generational. It is between insiders and outsiders - and the young are overwhelmingly outsiders.

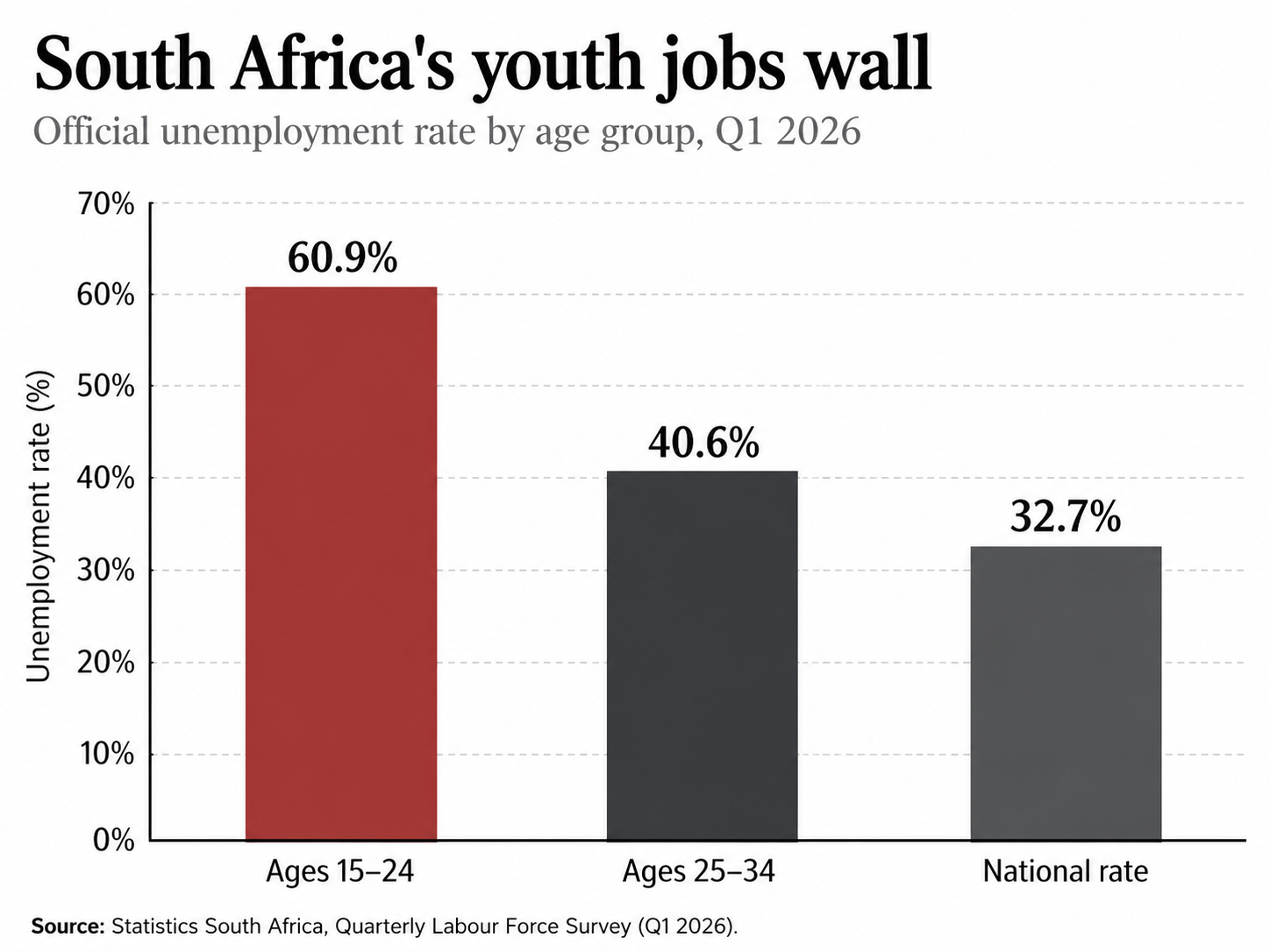

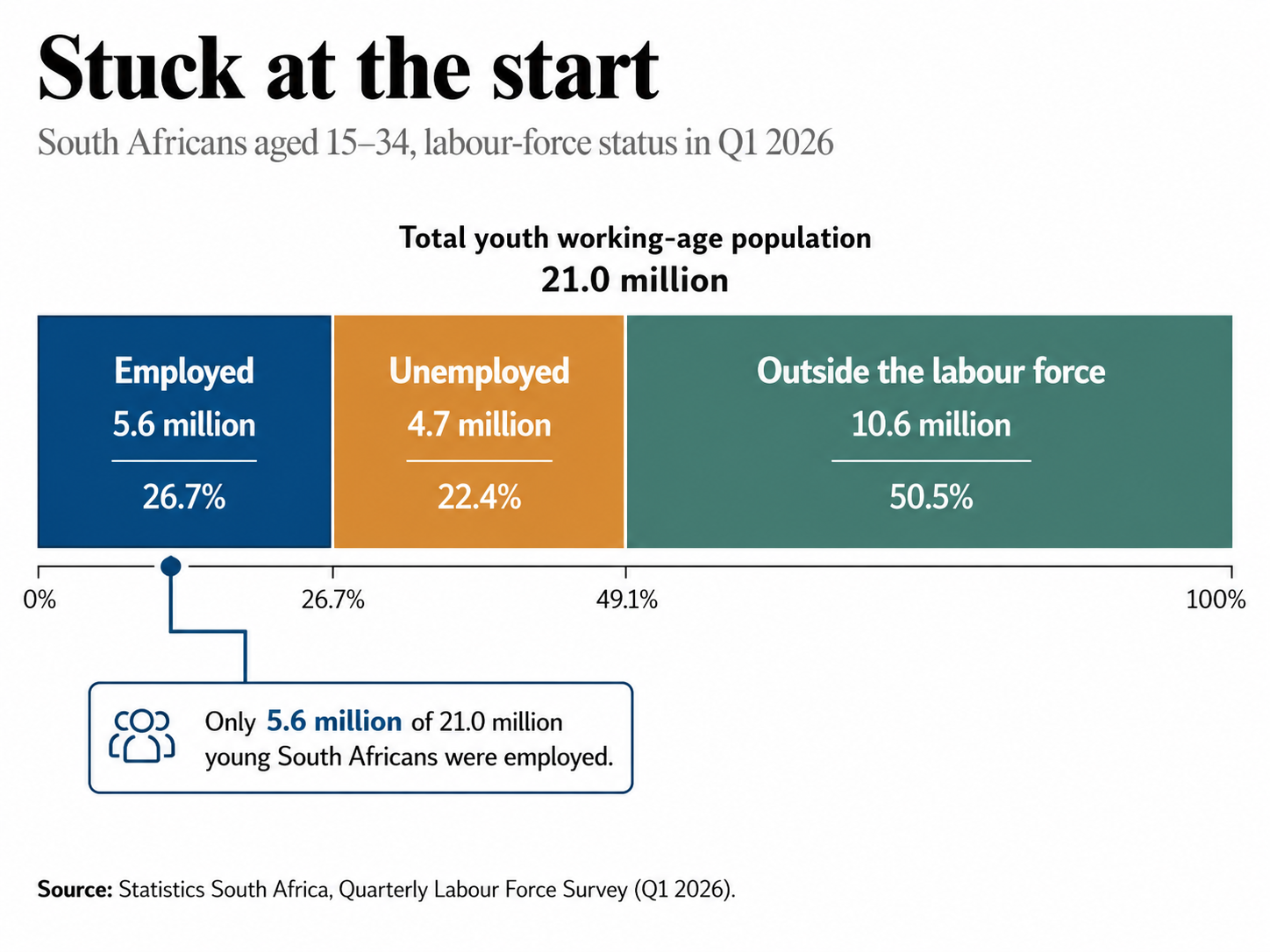

This is where the case becomes genuinely grim. In the first quarter of 2026, unemployment was 60.9% among South Africans aged 15 to 24 and 40.6% among those aged 25 to 34, against a national rate of 32.7%. Of the approximately 21-million people aged 15 to 34, only 5.6-million were employed. Another 4.7-million were unemployed and 10.6-million were outside the labour force.

That is not an awkward transition into adulthood. It is mass economic exclusion.

A young South African who cannot obtain a first job cannot acquire experience, contribute to a pension, qualify for a mortgage, establish a credit history, or begin the slow business of accumulating capital. The greatest advantage enjoyed by an older employed person is not necessarily that he has stolen anything from the young. It is that he was allowed onto the escalator before it stopped moving.

So, is there a financial war on the youth?

Not in the sense Galloway implies. There is obviously no grey-haired high command meeting secretly to raise house prices, reduce entry-level employment, and ensure the grandkids remain in the spare room. Much of what appears to be generational greed is ordinary life-cycle accumulation, demographic change, and the entirely reasonable desire not to be destitute in old age.

But South Africa has constructed something almost as damaging: an economy that protects people once they are inside while making entry extraordinarily difficult.

Formal workers receive labour protections and pension deductions. Property owners benefit from scarcity. Established businesses navigate regulation more easily than new ones. Universities ration places. The state has built a reasonably effective floor beneath old age, but no reliable bridge between school and work.

The problem is therefore not that South Africa does too much for the old. It is that it does catastrophically too little to help the young become economically adult.

The sensible response is not to cut the old-age grant or resent pensioners. It is to build housing where jobs exist, repair basic education, expand apprenticeships and vocational routes, reduce the risks and costs of hiring inexperienced workers, and generate the economic growth without which the rest is rearranging demographic deckchairs.

Horace described the old as being inclined to praise the years of their own youth while criticising the young. That remains one of ageing’s most persistent pleasures.

But the young are not imagining South Africa’s economic failure. They may exaggerate the conspiracy, misunderstand the causes, and occasionally believe that filming themselves discussing capitalism constitutes productive employment. Yet they are looking at an economy in which millions have been denied a first step.

The kids may indeed be alright. But the entry-level economy appears to have died before it got old. 💥

From the department of the understudy who steals the show...

From the department of crime-as-a-service, hold the criminal...

From the department of good news arriving by clerical accident...

Thanks for reading - please share if you have a friend (or enemy!) you think would value this blog and ask them to add their email in the block below - it's free for the time being. If the sign-up link doesn't appear, you'll find it on the site.

Till next time. 💥